Those that serve our country deserve professionals to serve them.

Dedicated to guiding military members in achieving their financial goals.

Military Experience

Choose an advisor with decades of experience with military pay and bonuses. After 26 years in the Navy, and getting six different bonuses, I know how they are paid, and how to structure your investments to take advantage!

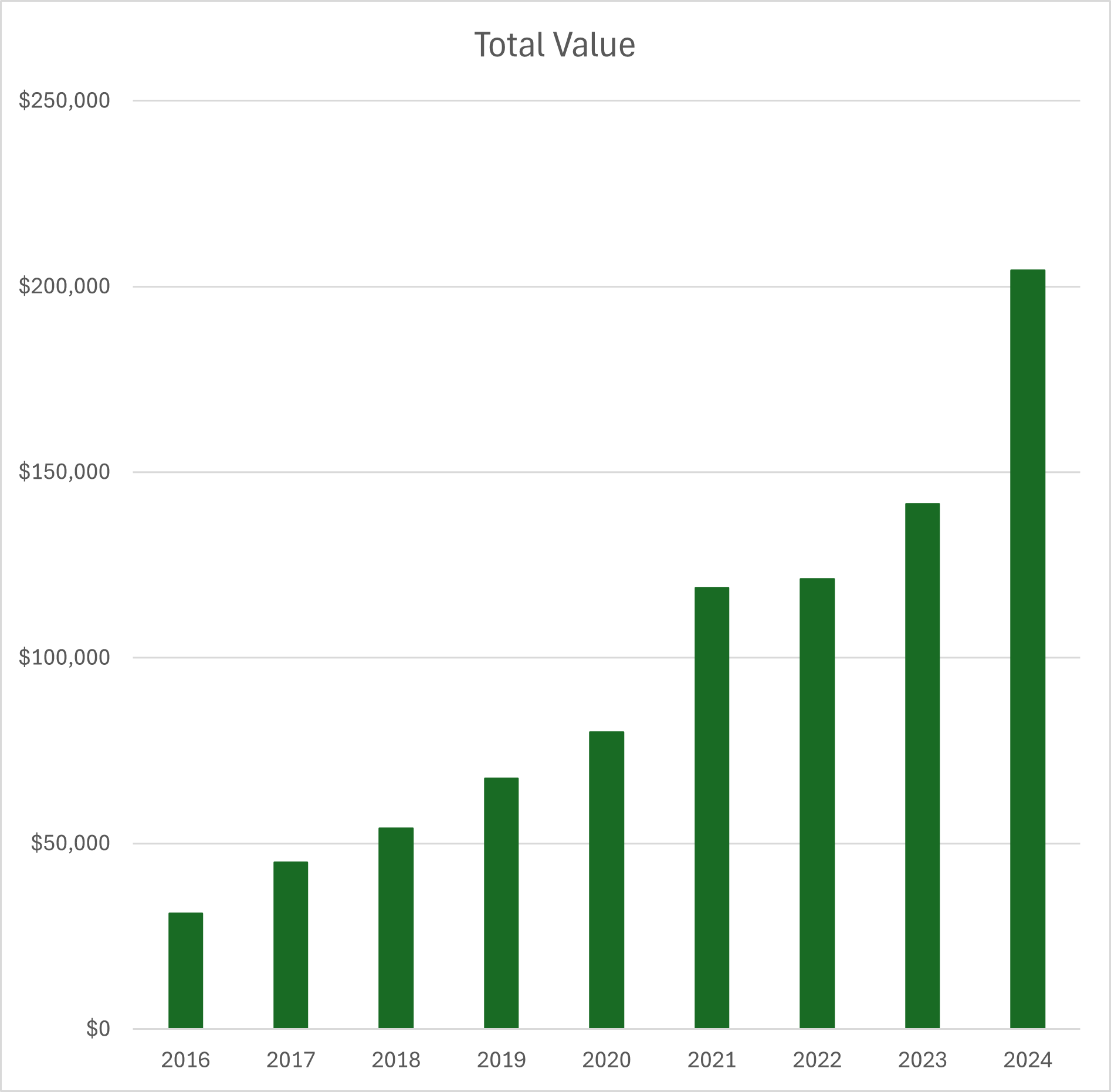

STAR Reenlistment Investing (Navy Nukes)

Here is a hypothetical example of how your STAR reenlistment and Zone B bonus would have grown over the last 8 years! This is assuming an SRB A (STAR) of 80,000, and SRB B of 50,000 with reenlistment dates at the 2 year and 1 month point and 6 year and 1 month point. Growth based on the SPY index fund less any dividend. Dates used are the beginning of November. Past results are not a guarantee of future growth. Market return may not be appropriate for all risk tolerances.

Far More Than Just Investing

It's not just about stocks, I'm here to help you navigate TSP, SDAP (Nuke Pay), maximize your reenlistment bonus, help you avoid pitfalls with buying a house or car and more! About to separate or retire? I can help with the transition in either circumstance.

Why Choose Us?

Why me? Well, it's simple, other than my passion for finances, it can be difficult to impossible to manage your money underwater or deployed to a desert!

Military Frequently Asked Questions

Here are some common questions we hear about financial planning for our military members.

Should I choose a Roth or Traditional TSP?

This choice is about when you want to pay taxes—now or later.

- Roth TSP: You pay taxes on your contributions today, but your withdrawals in retirement are tax-free.

- Traditional TSP: You contribute pre-tax dollars today, lowering your taxable income now, but pay taxes when you withdraw in retirement.

For many servicemembers early in their careers, income and tax rates may be lower than they are later in life. As a result, some individuals may find the Roth TSP attractive because contributions are taxed now rather than at withdrawal.

As income increases over time—through promotions, longevity increases, or large bonuses—the Traditional TSP can become more attractive, since it reduces taxable income in higher-earning years.

A simple way to think about it:

- Lower income years → Roth tends to be more favorable

- Higher income years → Traditional becomes more attractive

There is no universal rule, and the right choice can change over your career. Many servicemembers revisit this decision after major pay changes, promotions, or large bonuses.

Whether a Roth or traditional TSP is more appropriate depends on an individual’s current tax situation, expected future income, retirement goals, and other personal circumstances.

How is my bonus taxed?

Federal Income Tax

Your bonus is withheld at a flat 22% for federal income tax.

FICA (Social Security + Medicare)

Your bonus is also taxed with:

6.2% Social Security

1.45% Medicare

Total FICA: 7.65%

State Income Tax

Your state of legal residence determines whether state tax is withheld. Examples:

Texas: No state income tax

South Carolina: State tax is withheld

Important note

This is withholding, not your final tax bill. Your actual tax owed is calculated when you file your return — the withholding just pre‑pays part of it. Most servicemembers, especially early in their careers, have a lower effective tax rate, so much of these taxes will be returned when you file.

Journey Asset Management LLC does not provide tax advice or tax preparation services. When tax considerations arise as part of the financial planning process, we encourage clients to consult with a qualified tax professional. With the client’s permission, we are happy to work alongside the client’s tax advisor to help ensure coordination between financial and tax planning strategies.

How much should I put in TSP?

Deciding how much to contribute to your TSP depends on a variety of individual factors, including your financial goals, other savings and investments, current cash flow needs, and tax considerations.

As a starting point, contributing 5% to receive the full 5% Blended Retirement System (BRS) match is one way to help maximize this benefit—assuming you are under BRS and not legacy High-3. That is a 100% match on your first 5% once you’ve completed two years of service.

Beyond that, you may want to consider your overall retirement savings strategy:

- If you have a Roth or Traditional IRA: You may wish to prioritize maximizing those accounts next, since IRAs generally offer a wider range of investment options and greater flexibility.

- If you don’t have other retirement accounts: A contribution rate around 15% of your income (including the 5% match) is a common benchmark that may be appropriate for many servicemembers, though your situation may warrant a different rate.

Your appropriate contribution level can change over time as your income, benefits, financial situation, and goals evolve.

This information is for general educational purposes only and is not intended as financial, tax, or investment advice. Please consult with your financial professional to determine the contribution level that may be appropriate for your individual circumstances.

What should I invest in inside the TSP?

The appropriate investment allocation depends on a variety of factors, including your risk tolerance, time horizon, financial goals, and overall financial situation. There is no single allocation that is suitable for every investor.

One way some investors choose to allocate their TSP accounts is by combining the C, S, and I Funds to gain exposure to large U.S. companies, smaller U.S. companies, and international markets. For example, an investor seeking a growth-oriented allocation might consider the following:

Illustrative Example Only

- C Fund – 65%

- S Fund – 15%

- I Fund – 20%

This example is provided solely for educational purposes to demonstrate how the TSP funds can be combined to create a diversified allocation. It is not intended as a recommendation and may not be appropriate for your individual circumstances.

Generally:

- The C Fund provides exposure to large U.S. companies.

- The S Fund provides exposure to smaller U.S. companies.

- The I Fund provides exposure to international companies.

Before selecting an investment allocation, investors should consider their objectives, risk tolerance, time horizon, and other investments and consult with a qualified financial professional if needed.

A quick clarification

Many servicemembers think “retirement” means reaching the 20-year military retirement milestone, but retirement planning for investment accounts is a separate consideration. For example, a 40-year-old servicemember may still have many years before needing to access TSP assets.

As your time horizon, financial goals, or risk tolerance change, you may wish to review your investment allocation to determine whether it continues to align with your circumstances.

How do I invest my reenlistment bonus?

There’s no single “right” answer — it depends on your goals, your financial situation, and what you can realistically support. A reenlistment bonus is a powerful tool, and there are several smart ways to use it depending on what you need most.

Here are the three most common (and effective) approaches:

Option 1 — Long‑Term Planning

Some individuals use a reenlistment bonus to strengthen their long-term financial position by:

- Contributing to a Roth or Traditional IRA

- Using the bonus to help offset living expenses while increasing TSP contributions

- Investing through a taxable brokerage account

This approach may be considered by individuals who have established emergency savings, manageable debt levels, and a long-term investment horizon.

Option 2 — Debt Reduction

Some individuals choose to use a reenlistment bonus to reduce outstanding debt and improve monthly cash flow by:

- Paying down high-interest debt, such as credit cards or personal loans

- Reducing other debt obligations, such as vehicle or student loans

The potential benefit of debt reduction will vary depending on factors such as interest rates, loan terms, and overall financial goals.

Option 3 — Generate Income

Some individuals may choose to invest a reenlistment bonus in investments designed to generate income, such as:

- Dividend-paying funds

- Broad-market ETFs

- Other income-oriented investment strategies

The suitability of any income-focused strategy depends on an investor’s objectives, risk tolerance, and overall financial plan.

Before making decisions regarding a reenlistment bonus, investors should consider their individual circumstances and consult with a qualified financial professional as appropriate.

Common Considerations

When deciding how to use a reenlistment bonus, it may be helpful to consider whether the expenditure supports your long-term financial goals and overall financial situation.

Examples of uses that may warrant additional consideration include:

- Purchasing a vehicle that significantly increases monthly expenses

- Lifestyle upgrades that create ongoing financial commitments

- Home improvements that may not align with your financial priorities

- Using the bonus as a home down payment before establishing adequate savings or addressing other financial needs

Because every situation is different, there is no single “best” use for a reenlistment bonus. Evaluating how a decision may affect your long-term financial goals, cash flow, savings, and debt obligations can help you determine whether it is appropriate for your circumstances.

Start Your Financial Journey Today

Ready to take your finances to the next level? Contact us for a personalized consultation tailored to your needs.